Engineers and constructors adapt to serve an industry in transition.

Michael T. Burr, Public Utilities Fortnightly

From gas pipelines to PV arrays, the nation’s contractors are seeing growth in utility infrastructure. Fortnightly talks with executives at engineering and construction firms to learn what kinds of projects are moving forward, where they’re located, and what lies over the horizon.

Byline:

By Jack Azagury, Walt Shill, and Ted Walker

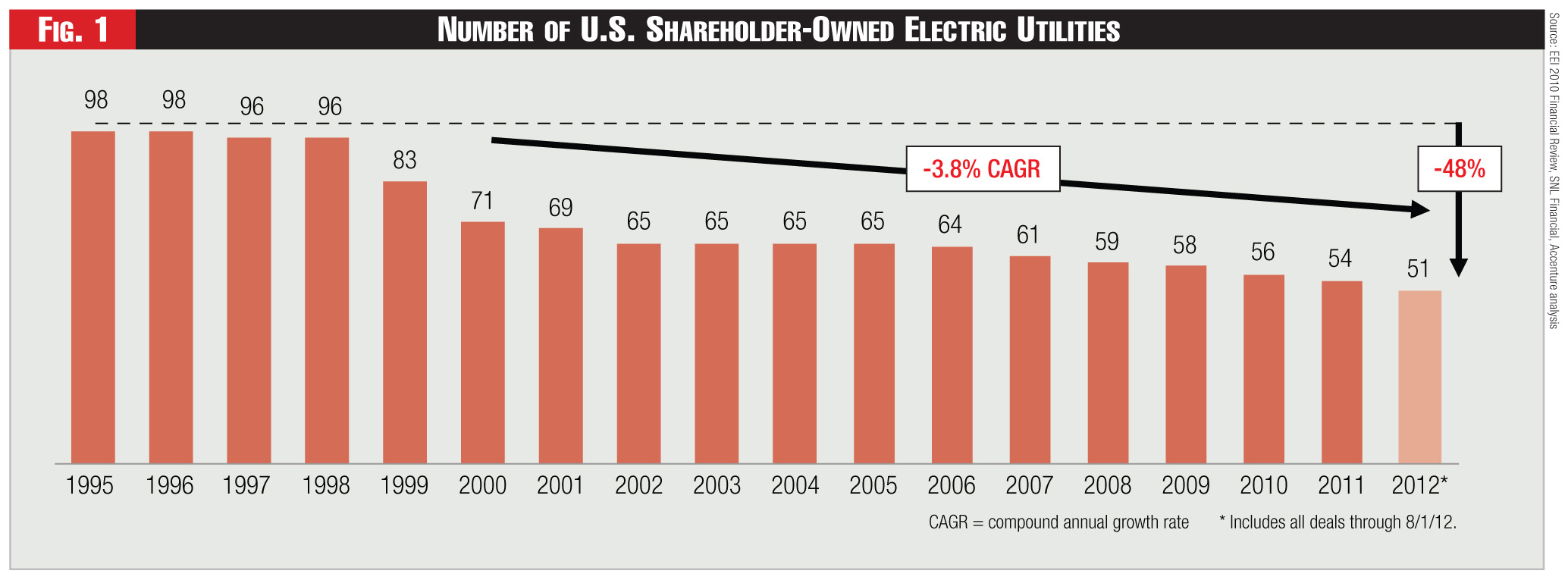

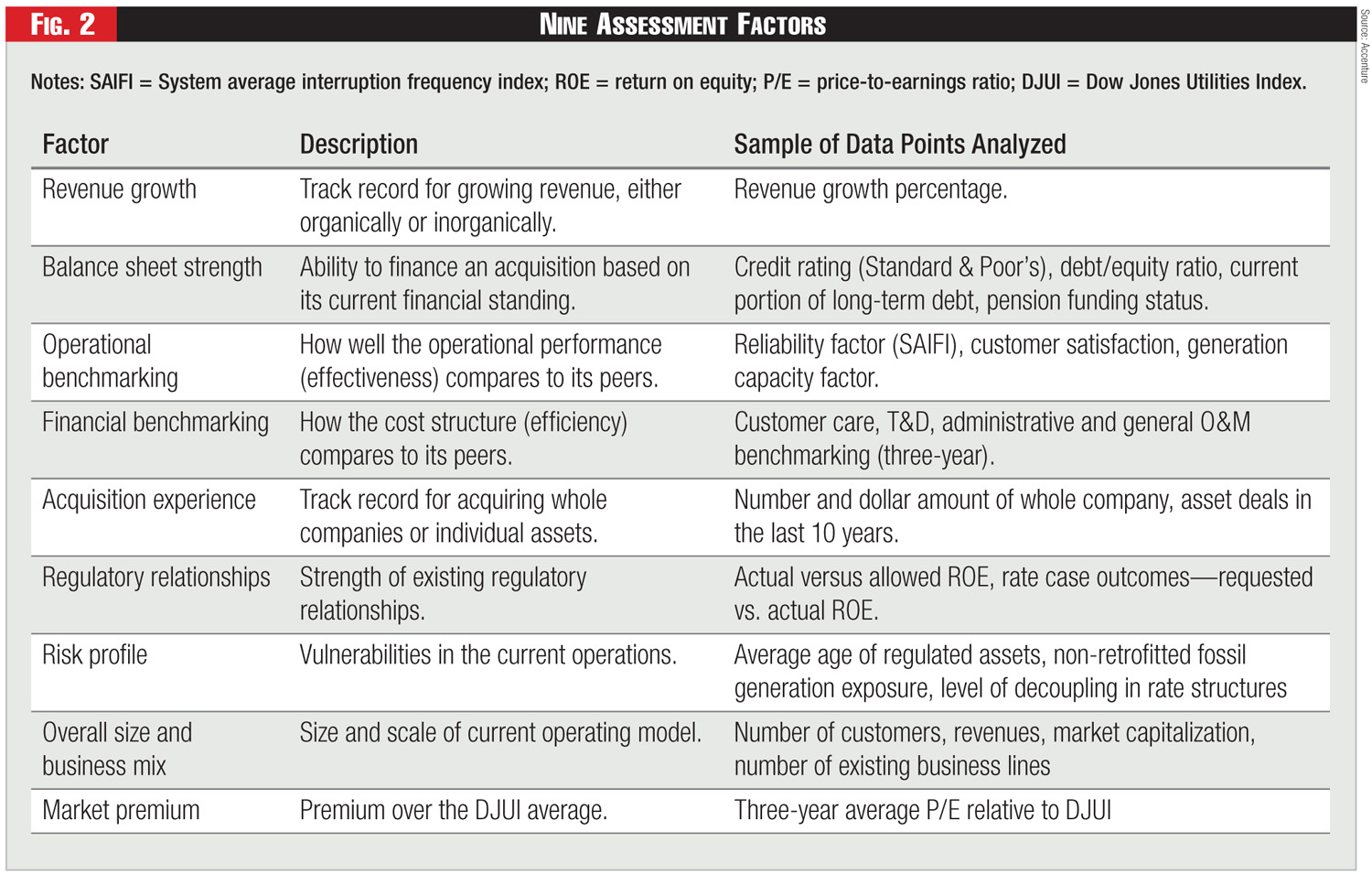

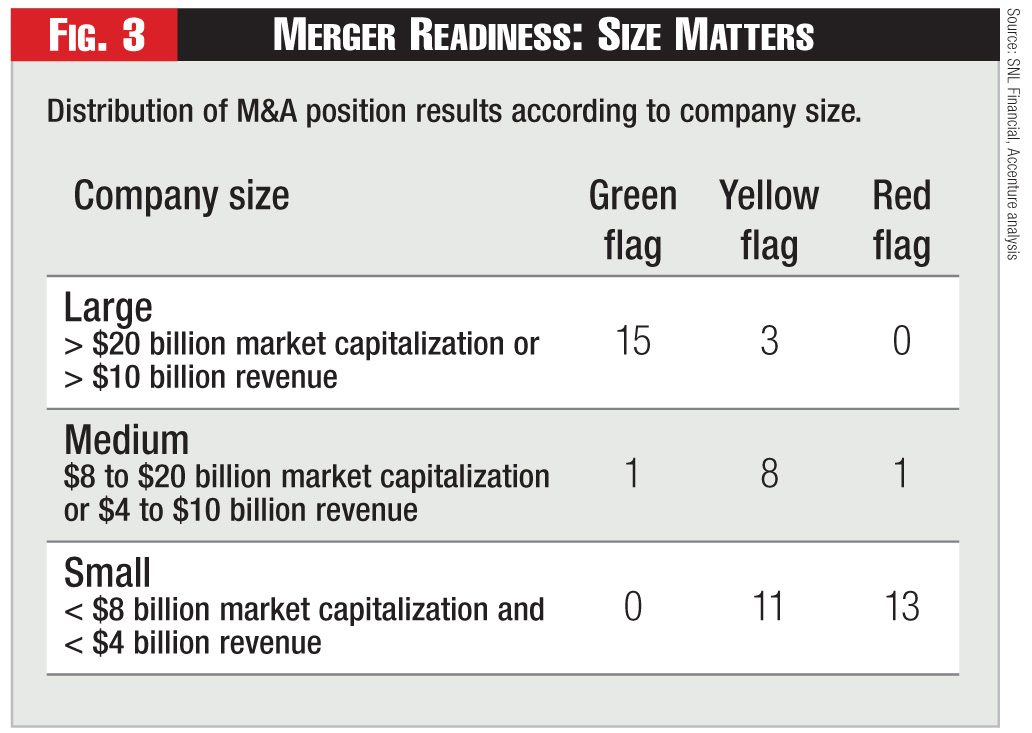

The industry’s slow-and-steady pace of mergers seems to be picking up speed, as larger and well-positioned players overtake smaller and weaker targets. Realizing the greatest value from consolidation requires companies to assess their strengths and weaknesses and focus on performance improvement—both before and after a deal gets done.

Author Bio:

Jack Azagury (jack.azagury@accenture.com) is Accenture’s North American Management Consulting lead for the resources industries, and Walt Shill (walt.shill@accenture.com) is global senior director at the company. Ted Walker (ted.h.walker@accenture.com) is a senior manager in the Accenture Utilities Strategy group. The authors acknowledge contributions from Jan Vrins, Accenture Utilities Management Consulting group, and Jason Allen, Accenture Research.

Positioning to win in the contest for scale.