Conditions are ideal for utility financing—but not forever. Although interest rates remain low, policy changes weigh on capital structures.

Image:

Sidebar:

Sidebar Title:

Pay It Forward

Sidebar Body:

One way that some utilities have been getting ahead of market changes is by issuing equity to pre-fund costs they expect to incur later. This generally takes two forms: equity forward contracts, and mandatory convertible offerings. Examples include Pepco Holdings, which sold about $350 million in shares on a forward basis in March, and PPL, which sold about $270 million in April. Also, NextEra Energy issued $600 million in three-year, mandatory convertible bonds on May 1, and another $650 million in September.

Both approaches carry a premium, but they allow utilities to capture today’s high stock prices in a forward sale. And some issuers have found banks hungry enough to participate in equity deals that they’ll take a substantial haircut for the opportunity. (See “BofA loses $12m on bought convert,” IFR 1932, May 2012.)

However, terms likely will normalize as soon as the current confluence of forces drives utilities back into the equity markets in earnest.–MTB

Author Bio:

Michael T. Burr is Fortnightly’s editor-in-chief. Email him at burr@pur.com.

Bond investors are keen for signs of a legitimate recovery, and will be looking to move into holdco bonds.

Category:

Op Ed

Author Bio:

Josh Olazabal is a vice president in the credit research group at PIMCO’s Newport Beach office. Previously he was a consultant with McKinsey & Co., and worked in corporate development at Duke Energy before that.

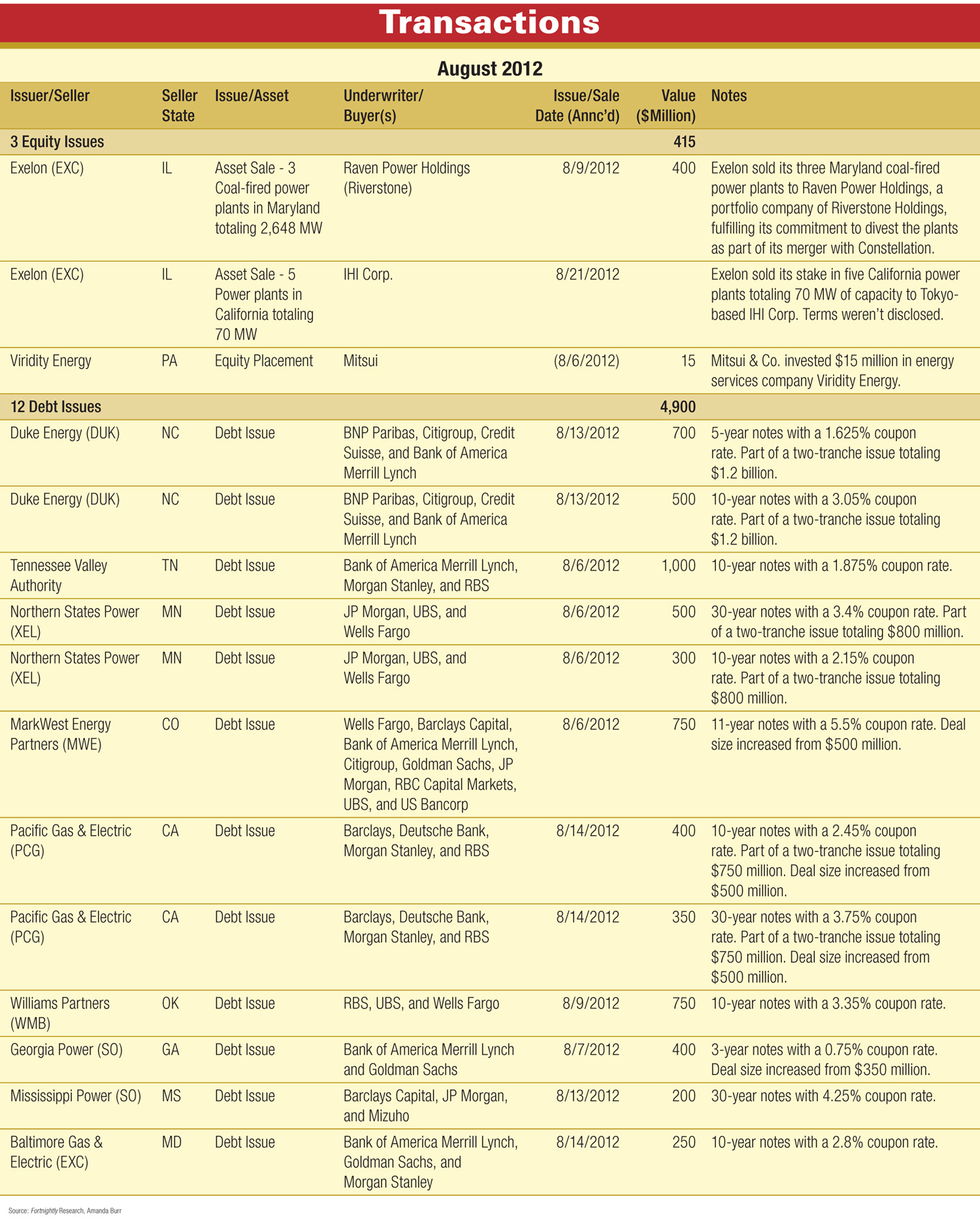

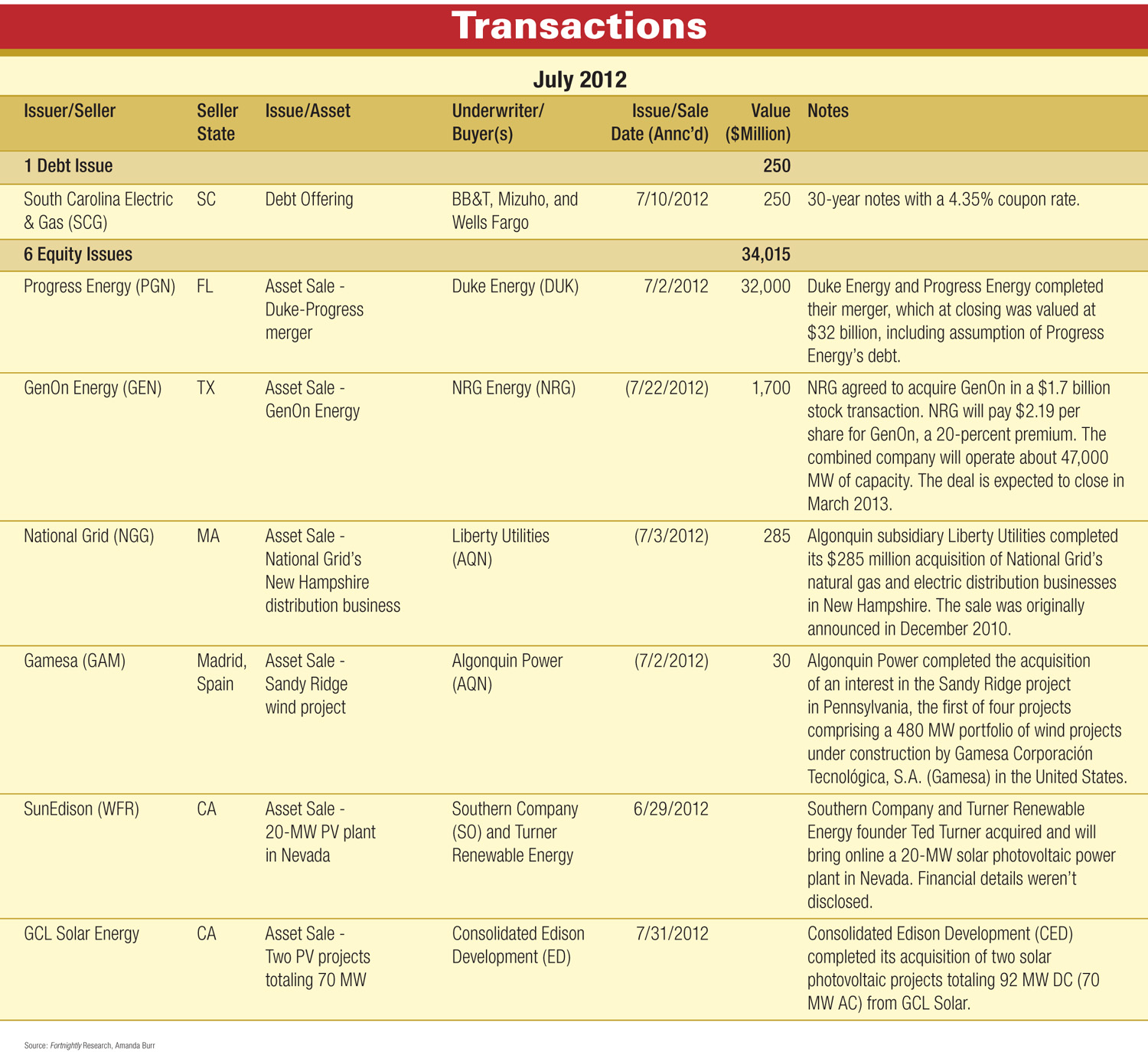

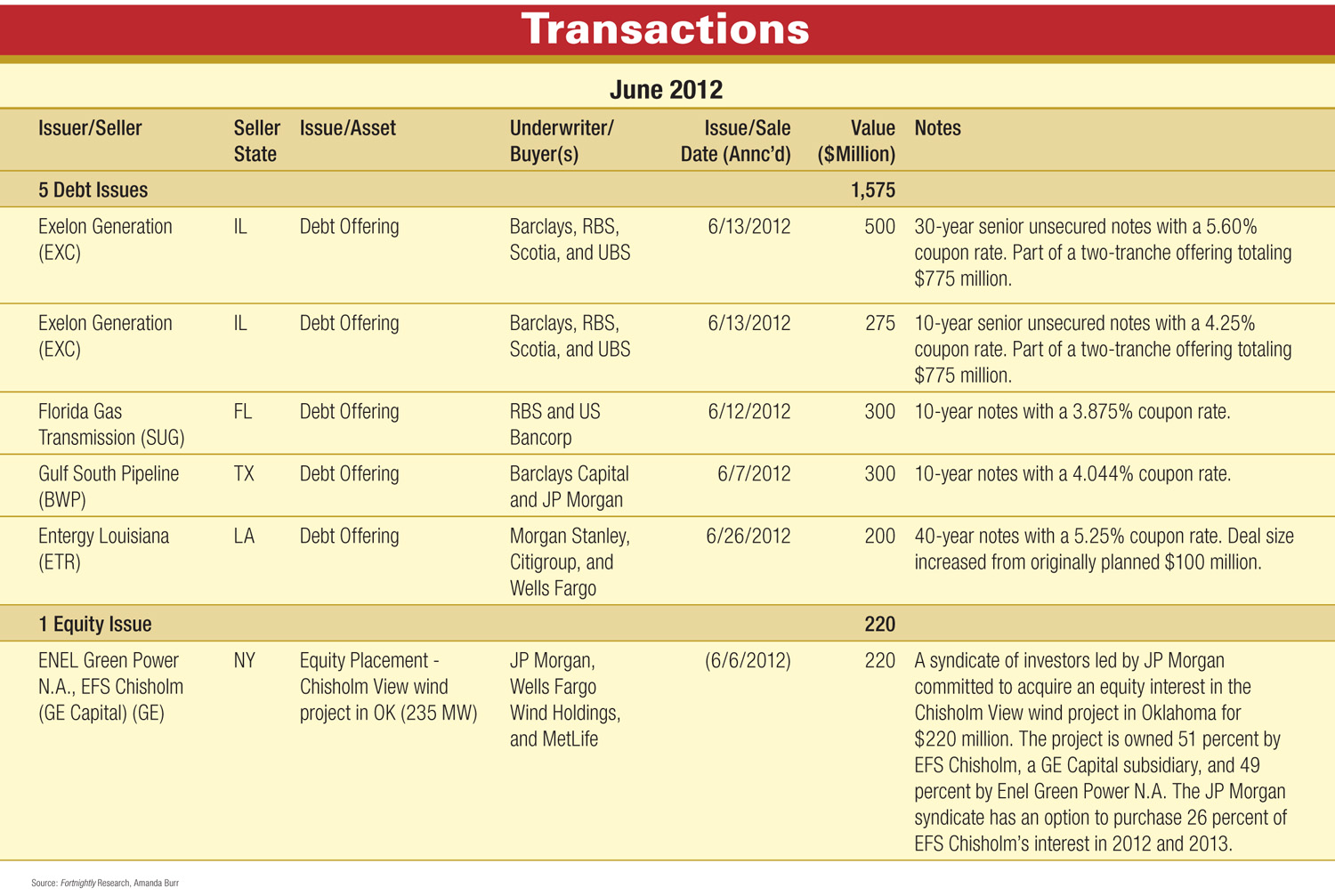

Duke and Progress complete their merger; NRG agrees to acquire GenOn; Algonquin acquires National Grid's New Hampshire distribution business, and acquires an interest in Gamesa's Sandy Ridge wind project; plus other equity and debt transactions, totaling more than $34 billion.

")