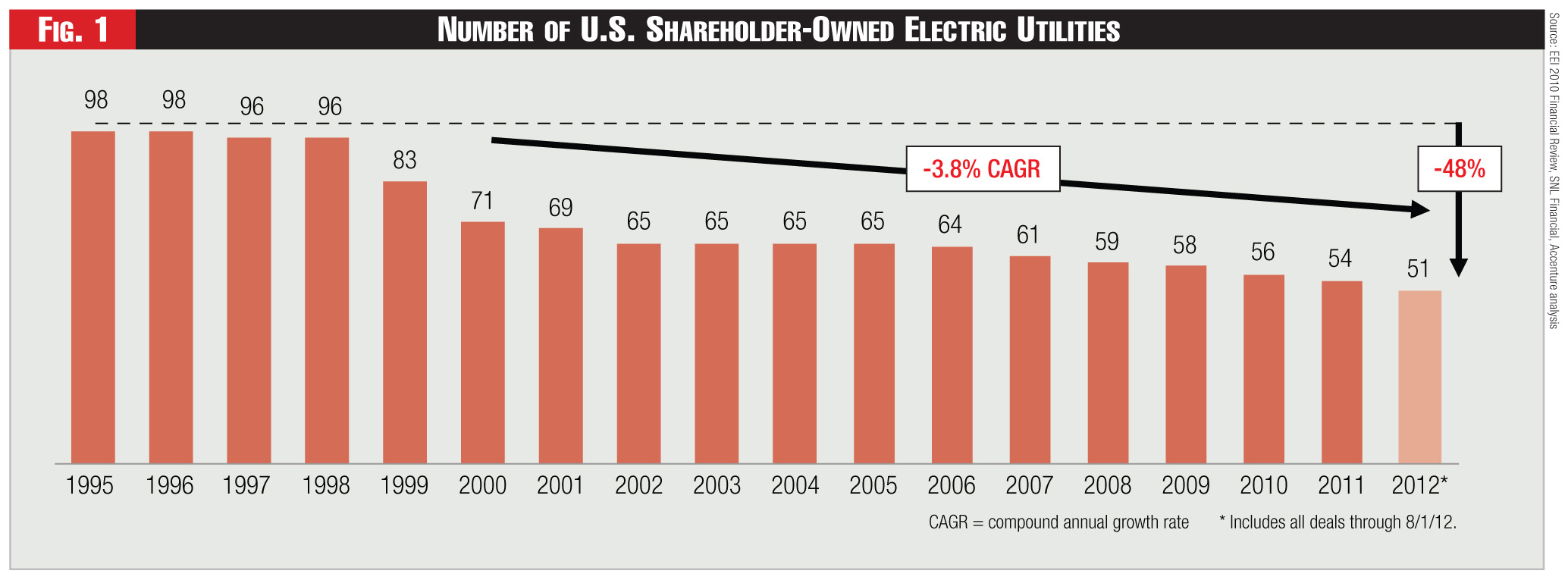

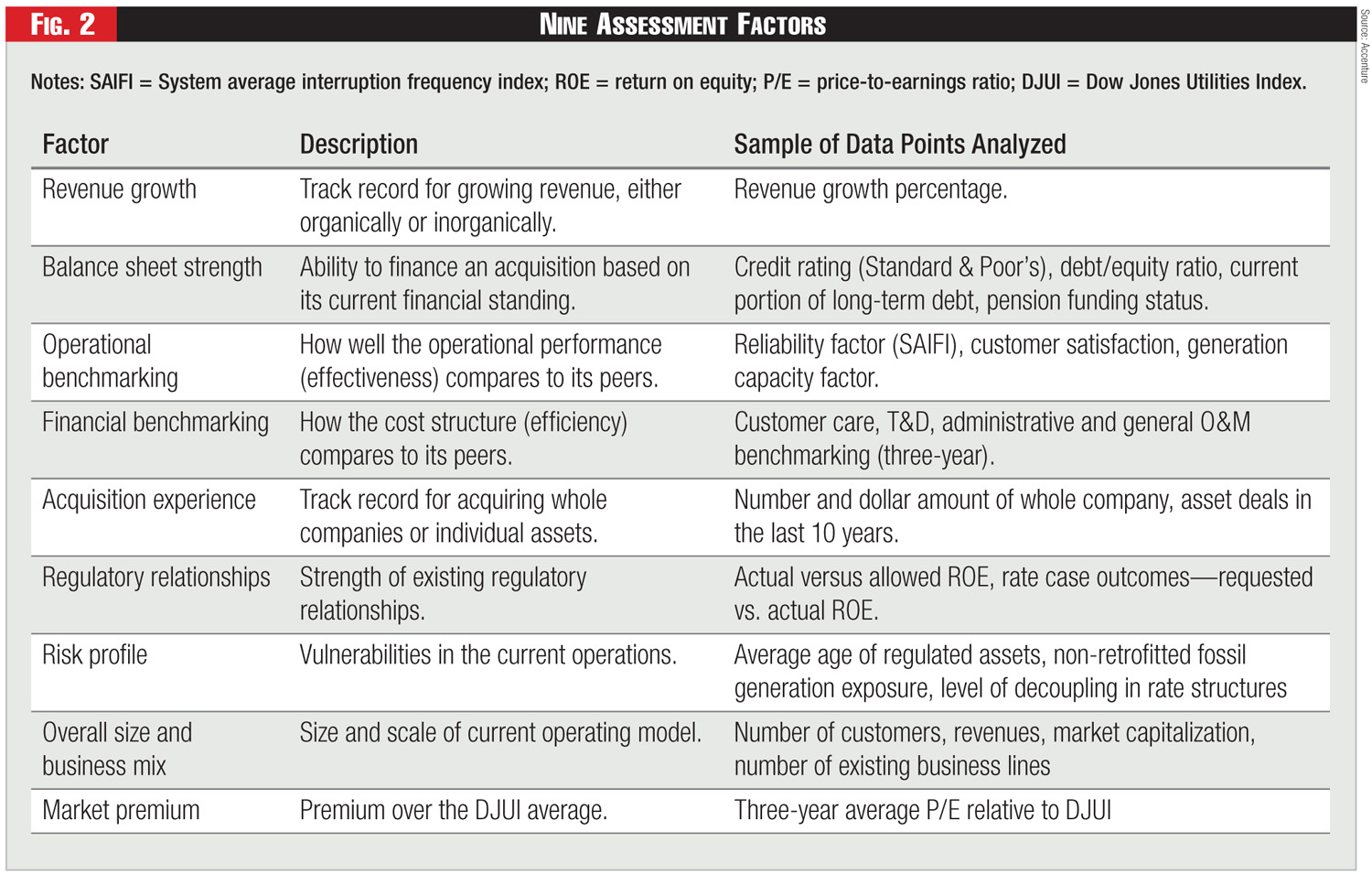

(September 2012) Our annual financial ranking shows some remarkable shifts among the industry’s shareholder value leaders. Despite flat demand and low commodity prices, investor-owned utilities are investing heavily in capital assets. Investment discipline and operational excellence distinguish leaders on the path to financial performance.

Category:

The <i>Fortnightly 40</i> Best Energy Companies